The world’s largest carmakers could face a potentially crippling shortage of aluminium, as China’s power crisis threatens supplies of a key component used to make the lightweight metal. Magnesium is an essential raw material for the production of aluminium alloys, which are used in everything from gearboxes, to steering columns, seat frames and fuel tank covers. Owing to production curbs in China, which has a near monopoly on the magnesium market, stockpiles of the metal are running dangerously low across Europe. “There are no substitutes for magnesium in aluminium sheet and billet production,” said Barclays analyst Amos Fletcher in a report. “Thirty-five per cent of downstream demand for magnesium is auto sheet — so if magnesium supply stops, the entire auto industry will potentially be forced to stop.” Canadian metals company Matalco told its clients last week that magnesium availability had “dried up”, and if the scarcity persisted it would have to curtail output of aluminium billet next year, according to a report by S&P Global Platts. The warning from Matalco shows how the power crisis in China is affecting global supply chains, driving up the price of key industrial materials and fuelling concerns about inflation.

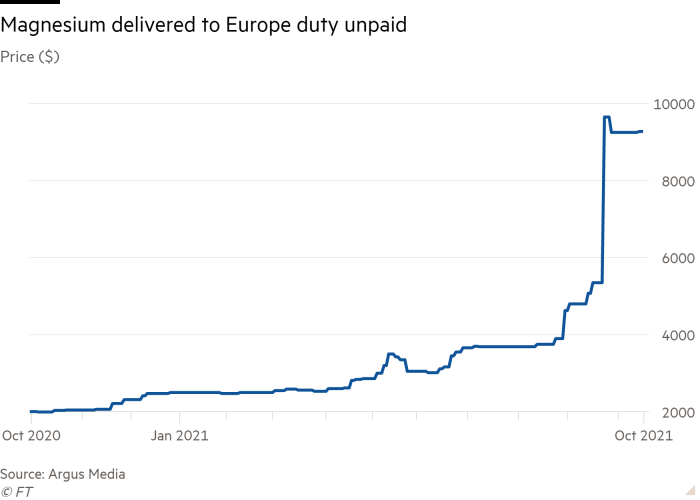

While a shortage of semiconductors has been the main issue facing the automotive industry this year, the focus is now shifting to magnesium, which increases the strength of aluminium when added as an alloying agent. “A magnesium shortage could trigger a shortage of [usable] aluminium, which in turn could also hit car production,” said analysts at BofA Securities in a report. “We stress at this point that such a scenario is not yet included in our estimates. The issue has just emerged and no carmaker has yet warned about it.” Around 85 per cent of the world’s magnesium production comes from China, and a large chunk of it from one town in Shaanxi province, Yulin. About a month ago, the local government ordered roughly 35 of its 50 magnesium smelters to close until the end of the year and told the rest to cut production by 50 per cent in order to hit energy consumption targets. To produce one tonne of magnesium takes 35-40 megawatt hours of power, versus aluminium at 16 MHW, according to BoA Securities. As the metal is difficult to store — it starts to oxidise after three months — stocks could run critically low before the end of the year if China does not crank up production. This has been reflected in prices, with magnesium imported in Europe surging 75 per cent over the past month to a record high above $9,000 a tonne, according to Argus Media, a price assessment company. In a statement issued earlier this month, WV Metalle, Germany’s non-ferrous metal trade association, called on its government to initiate diplomatic talks urgently with China. “It is expected that the current magnesium reserves in Germany and throughout Europe will be exhausted in a few weeks at the end of November 2021 at the latest,” the statement said. “In the event of a supply bottleneck of this magnitude, there is a risk of massive production losses.” Other industry groups have also raised the alarm. European Aluminium, whose members include Norsk Hydro, Rio Tinto and Alcoa, asked the EU and national governments to work urgently towards immediate actions with their Chinese counterparties. It fears Beijing will now direct the remaining production to its vast domestic aluminium industry. “The current magnesium supply shortage is a clear example of the risk the EU is taking by making its domestic economy dependent on Chinese imports,” EA said in a statement. “The EU’s industrial metals strategy must be strengthened.” Magnesium is already on the EU’s list of critical raw materials. European companies including Norsk Hydro used to produce magnesium but stopped because they could not compete with lower costs at Chinese producers. Unlike Europe, North America does boast one large domestic producer of metal, US Magnesium, which was offering a degree of protection said Stephen Williamson, research manager at commodities consultancy CRU. “Aluminium producers North America are also working their scrap supply chains very aggressively to make up for whatever raw magnesium they are not able to source.” The key question now is whether magnesium production in China will restart before the end of the year. Given the importance of aluminium to the country’s manufacturing sector it is reasonable to assume that resumption is imminent. “But this is a risk worth watching carefully,” said Barclays’ Fletcher.

Inventories are currently low across a number of metals. This is especially true of copper, where stocks available on the London Metal Exchange sunk to the lowest level since 1974 last Friday after a surge of orders. Copper rose 10 per cent last week and on Tuesday was trading at $10,300, not far from its record price of $10,747 reached in May. Over the past month copper not already earmarked for withdrawal from LME warehouses has plunged to just 15,225 tonnes, from more than 150,000 tonnes. Putting that figure in to perspective, about 25m tonnes of refined copper is consumed annually. In China, copper stocks on the Shanghai futures exchange have fallen to the lowest level since 2009. For the LME, the world’s biggest marketplace for industrial metals, dwindling copper stocks could present a problem because the exchange runs a contract that is settled physically if it is not closed out. “While some metal may make its way into the warehouse system, there may not be any immediate remedy, beyond perhaps a global economic slowdown, said Michael Widmer, commodities strategist at BofA Securities.

China’s magnesium shortage threatens global car industry

Production curbs in the country have hurt stockpiles of a key ingredient to make aluminium in vehicles