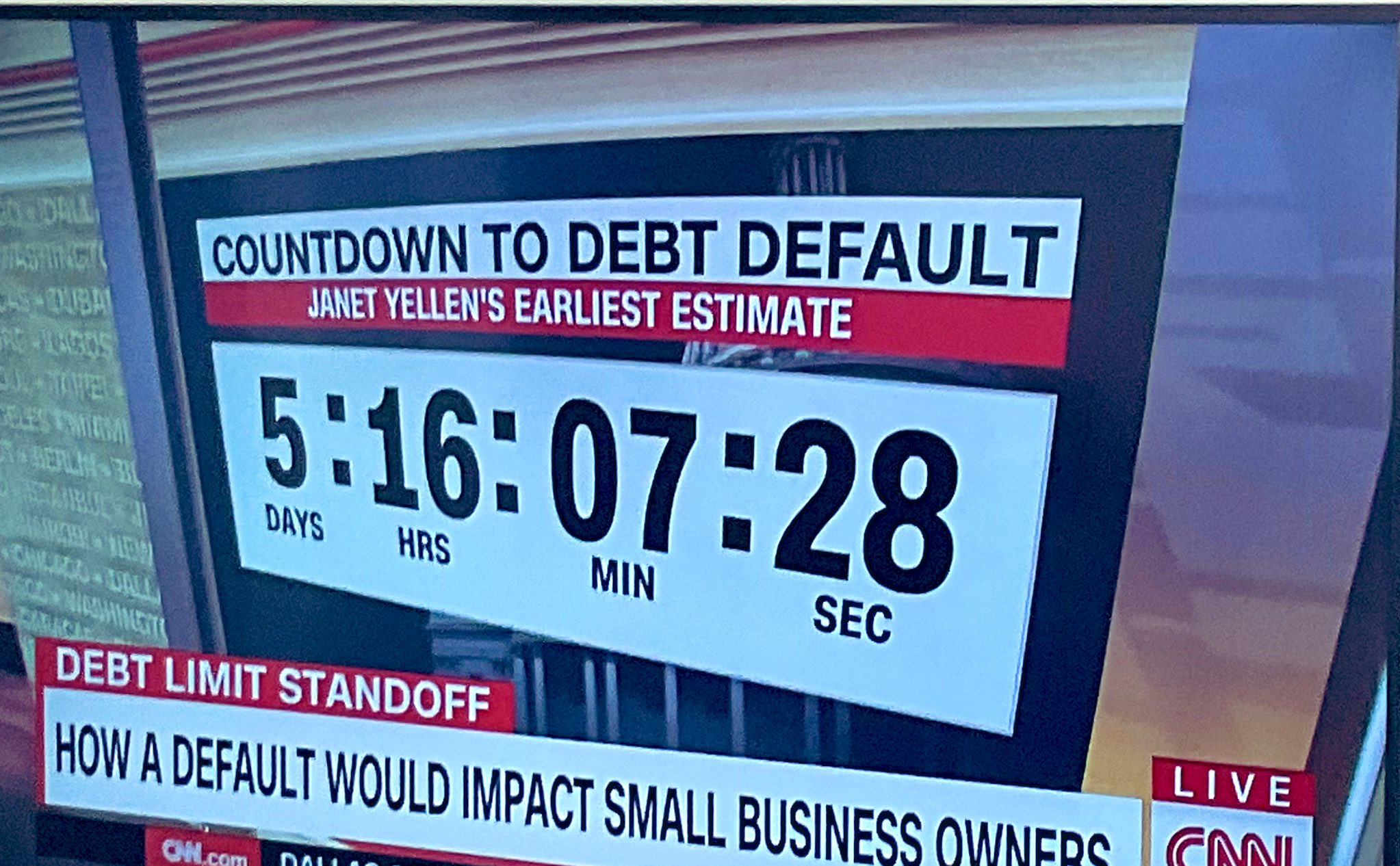

This deserves both anCountdown to Default for the US treasury:

and a

and a

Latest Thread

This deserves both anCountdown to Default for the US treasury:

and a Yeah UAE, SA are so reliable.Brilliant idea let's get money from those who will not boss us around.

Erdogan says Gulf states sent cash in relief for Turkey

Turkish President Tayyip Erdogan said on Thursday that Gulf states recently sent funding to Turkey, briefly helping relieve the central bank and markets, and he intends to meet and thank their leaders after Sunday's runoff presidential election.www.reuters.com

How about admitting that keeping the interest rates low is a bad idea?Get loans from the IMF or London loan sharks you mean?

How about admitting that keeping the interest rates low is a bad idea?

Also the IMF does not give out loans for nothing. These loans come with specific advice on measures to take to improve the economy. And when inevitably you have a country that takes the money, does not follow the advice given by the IMF and predictably their economy continues to tank, you have people looking to blame the big, bad IMF for the crime of...*gasp*...giving money to you with the assumption that you will be taking measures to improve your economy instead of admitting that you messed up and wasted their money.

Instead you propose that taking money from Gulf monarchies claiming that they will not "boss" Turkey around...ignoring that they have geopolitical conflicts with Turkey and absolutely will use their newfound influence over the Turkish economy to direct Turkey to abandon its geopolitical goals if it doesn't serve their goals. According to some, Qatar already does this, directing Turkey with one hand while stabbing it in the back with the other.

I swear, some people's dislike of anything to do with the West is so intense that you would open your doors to Satan if it would spite the West.

While you are writing this Turkish bureaucrats are begging London loan sharks on the orders of Erdogan, to lend them dollars with a %10+ interest rate. You are living high on copium.I don't dislike western people, I worked and lived with them for some years but I don't like the so called western capital that caused the collapse of the Ottoman Empire and also the previous to Erdoğan era Türkiye. We will not borrow their money anymore and before too long we may as well start lending.

You know very well that not borrowing from them means beyond what is required to roll the debt we owe them already. The debt stock does not go away overnight.While you are writing this Turkish bureaucrats are begging London loan sharks on the orders of Erdogan, to lend them dollars with a %10+ interest rate. You are living high on copium.

It wasn't the western capital that collapsed the empire, nor was the western capital the reason of the 90s crash. Bad internal management caused them both. Watch us going in for a third time.I don't dislike western people, I worked and lived with them for some years but I don't like the so called western capital that caused the collapse of the Ottoman Empire and also the previous to Erdoğan era Türkiye. We will not borrow their money anymore and before too long we may as well start lending.

No it won't. It will just strangle the market and cause more unemployment.Is all of this shit because the interest rate and Trump tweet ?

If tomorrow Erdogan raise the rate to 30% , would this solve the crisis ?

Will they send their armies to strangle us if we delay payments or will they order us around when we mind our business, I don't think so.We are being fixated on gulf for our economy and Russia for our energy. This will end horribly.

Neither will IMF, in that case. Maybe they send in Ethan hunt.Will they send their armies to strangle us if we delay payments or will they order us around when we mind our business, I don't think so.

If it was up to that youtuber we'd been collapsed countless times now. That man is not a reputable source.

incredible economic failure and they keep voting for it.

A couple comments on the inflation from the video.

"As someone currently living in Turkey (not Turkish), the official inflation figures are a joke. Since October I've seen the price of a bottle of Coke go from 14 lira to 27-30 lira, and since January 400g of beef mince went from low 40s to over 90 lira. These are only 2 of hundreds of examples. I'm glad I don't get paid in lira, but the poor locals are fucked. The only saving grace e is my rent is in lira, so I've seen my rent come down about 10% in real money..."

"Same man as a someone (non Turkish) living in Turkey Im blessed enough to be making a living outside of turkey but I feel extremely bad for the locals who live here it’s honestly baffling how fast and fucked up inflation is rising. I especially feel for those who just recently graduated looking for their first jobs. Not only will they start with a shit salary but they’ll most likely be contracted out without having their salaries adjusted for inflation and after years of hard work and study they’ll just end up struggling to even make rent by the end of the year. It’s truly disheartening. Like bro I was eating maxi XL menus at popeyes for 85 TL at the start of the year and now it’s at least 120 TL it’s just fucking wild to see."

If it was up to that youtuber we'd been collapsed countless times now. That man is not a reputable source.

They are being usefull but you don't want them to be usefull.Neither will IMF, in that case. Maybe they send in Ethan hunt.

Are you really this blind to see that with greater Russian and Gulf effect in our economy we are moving more in line with their own goals and not a third, our way? Soon you'll see, it'll be too late tho.

The "analysis" isn't his either, he's just parroting what has been already said by other "analysts."but he's never been sensationalists in his analysis

it’s definitely going to get worse

it’s definitely going to get worse