Latest Thread

- Bangladesh Bangladesh building first research vessel to explore the Bay

- Bangladesh Bangladesh to build 108-km fence along Myanmar border

- Forum Announcement Bug fixing

- UK BAE teaming up with Boeing, SAAB to offer T-7 for RAF

- Bangladesh News Govt Plans $7 Billion Military Modernisation Drive Over Next Decade: PM

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Bankrupt Banks

- Thread starter Bogeyman

- Start date

Why have they withdrawn their money though?

Silicon Valley's 'greed and avarice' have 'finally come home to roost' in SVB collapse, trader says

"Banking should be boring, a lot like watching paint dry — and any time it's not, you've got a problem," one investor told CNBC.

Regulators and auditors who’re driven by capitalism will fail. Should just have a robot (ai) monitor these banks. Robots would do a better job at regulating banks.

Silicon Valley's 'greed and avarice' have 'finally come home to roost' in SVB collapse, trader says

"Banking should be boring, a lot like watching paint dry — and any time it's not, you've got a problem," one investor told CNBC.www.cnbc.com

Regulators and auditors who’re driven by capitalism will fail. Should just have a robot (ai) monitor these banks. Robots would do a better job at regulating banks.

Ryder is entirely correct (at least in the underlying layer). It has far more to do with (anti-capitalist + corrupt) politics than capitalism.

Silicon valley is a deep blue democrat hub for a reason.

California at large has entrenched monopoly (Dem) party system in its city councils even....where there is near entire monopoly, there is no choice and there is no capitalism (which needs active political competition for there to be fair regulation and application of the law given sunshine of new administrations are the best disinfectant).

i.e The deepest layers of entrenched self-serving Democrat party malfeasance, corruption and incompetence have nothing to do with capitalism.

They are infact fairly anti-capitalist....even GOSPLAN-lite if you look at collaboration of corporates with big tech VC and the federal govt politicians....which inevitably push out natural market price signalling and consequences.

It is (increasingly) dystopic marxist corporatism.

Entirely anti-capitalist in both principle and application:

The (layer 1 cause) Biden debt-based spending splurge (using the already overleveraged ZIRP) of 2021-2022 (and showing no signs of stopping) creating ZIRP/QE that cause both inflation, bubbles and incentivizes bad investment by sheer liquidity pressure.

The (layer 2 cause) of unbridled DEI and ESG "focus" (and thus dereliction on what they are actually there for) of the corrupt marxists running this bank (and similar banks) created the inevitable spillover into frankly terrible bond buying decisions (on the premise I/R would not be increased by the fed)....combined with Fed going against the premise and causing the tinder for this bank run quite quickly (given the bonds recklessly bought by the bank last year can now only be sold at a loss)

The (layer 3 cause) FDIC intervention (after this bank run started) to go past the 250k insurance limit in "too big to fail" on the premise of marxist politicians inevitably helping out marxist corporatist-banker cabal, ignoring the 07/08 lessons yet again (in that the collective public should not be liable for irresponsible decisions of specific individuals).

There are further layers, sublayers and parallel layers (all found in the 08 crisis yet again)....but this will do for now.

Last edited:

Ryder is entirely correct (at least in the underlying layer). It has far more to do with (anti-capitalist + corrupt) politics than capitalism.

Silicon valley is a deep blue democrat hub for a reason.

California at large has entrenched monopoly (Dem) party system in its city councils even....where there is near entire monopoly, there is no choice and there is no capitalism (which needs active political competition for there to be fair regulation and application of the law given sunshine of new administrations are the best disinfectant).

i.e The deepest layers of entrenched self-serving Democrat party malfeasance, corruption and incompetence have nothing to do with capitalism.

They are infact fairly anti-capitalist....even GOSPLAN-lite if you look at collaboration of corporates with big tech VC and the federal govt politicians....which inevitably push out natural market price signalling and consequences.

It is (increasingly) dystopic marxist corporatism.

Entirely anti-capitalist in both principle and application:

The (layer 1 cause) Biden debt-based spending splurge (using the already overleveraged ZIRP) of 2021-2022 (and showing no signs of stopping) creating ZIRP/QE that cause both inflation, bubbles and incentivizes bad investment by sheer liquidity pressure.

The (layer 2 cause) of unbridled DEI and ESG "focus" (and thus dereliction on what they are actually there for) of the corrupt marxists running this bank (and similar banks) created the inevitable spillover into frankly terrible bond buying decisions (on the premise I/R would not be increased by the fed)....combined with Fed going against the premise and causing the tinder for this bank run quite quickly (given the bonds recklessly bought by the bank last year can now only be sold at a loss)

The (layer 3 cause) FDIC intervention (after this bank run started) to go past the 250k insurance limit in "too big to fail" on the premise of marxist politicians inevitably helping out marxist corporatist-banker cabal, ignoring the 07/08 lessons yet again (in that the collective public should not be liable for irresponsible decisions of specific individuals).

There are further layers, sublayers and parallel layers (all found in the 08 crisis yet again)....but this will do for now.

Credit Suisse’s Troubles Reignite Fears of Bank Contagion—and Drag Stocks Down

Problems at Switzerland’s second-biggest lender are causing stocks around the world to falter—and reigniting fears for the banking sector.

On Wednesday, Credit Suisse CS -20.12% ‘s top shareholder said in a Bloomberg interview that it wouldn’t invest additional money in the Swiss bank. Saudi National Bank Chairman Ammar Al Khudairy told the media outlet that taking a stake of more than 10% in Credit Suisse would trigger regulatory complications.

That pushed shares of Credit Suisse to a new low on Wednesday. The stock (ticker: CSGN.Switzerland) closed down 24% in Zurich and its American depositary receipts (CS) were down 25% in U.S. trading.

Credit Suisse has asked the Swiss National Bank SNBN –3.22% , the country’s central bank, and its financial regulator, Finma, to make a statement reassuring investors about its financial health, the Financial Times reported, citing unidentified people familiar with the talks. Credit Suisse and the Swiss National Bank declined to comment on the report.

The U.S. Treasury Department is actively reviewing the U.S. financial sector’s exposure to Credit Suisse, according to a Bloomberg report. The Treasury Department didn’t respond to a request for comment

After Silicon Valley Bank’s collapse, the banking sector is on high alert. European banks such as France’s Société Générale (GLE. France) and Italy’s UniCredit (UCG. Italy) were down double-digits Wednesday. UBS Group (UBSG.Switzerland) fell nearly 8.7%.

Shares of U.S. lenders Citigroup C –5.47% (C), JPMorgan Chase JPM –4.46% (JPM), and Wells Fargo (WFC) also fell on Wednesday.

Shares of the regional banks put on downgrade watch by ratings agency Moody’s on Tuesday were mixed. Western Alliance Bankcorp (WAL) and Comerica (CMA) stock were down earlier, but have since turned higher. Shares of First Republic Bank (FRC) have fallen 17%.

Renewed fears of contagion hit the broader market too. The S&P 500 SPX –0.81% was off 2% and the Dow Jones Industrial Average was down more than 700 points, or 2.2%. At one point, the S&P 500 fell into negative territory for the year. The pan-European STOXX Europe 600 index was down nearly 3% with all but 45 components in the red.

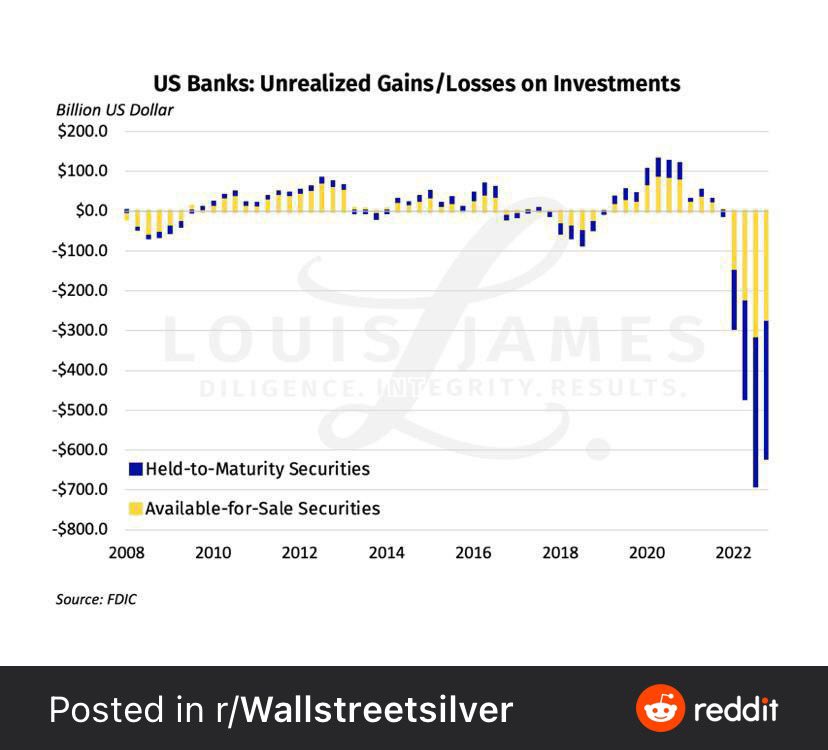

“The banking rout has taken on another ominous twist,” said Susannah Streeter, head of money markets at Hargreaves Lansdown. “The worry is that banks sitting on large unrealized losses in their bond portfolios might not have sufficient buffers if there is a fast withdrawal of deposits.”

Investors are watching coming policy decisions at central banks, which—in some cases—have raised interest rates aggressivly over the past year. The European Central Bank, set to meet Thursday, will be the first central bank to meet since SVB’s meltdown. The Federal Reserve meets on March 22.

European Central Bank President Christine Lagarde said a month ago that the ECB intends to increase rates by another half point in March. Odds that the Fed will not raise rates at the March meeting have increased to nearly 60% Wednesday, according to the CME FedWatch.

Why Is Credit Suisse Struggling? A Recap of Recent Troubles.

Credit Suisse’s struggles extend beyond today’s news.The stock fell on Tuesday after it released a delayed annual report that described weaknesses in the firm’s financial controls. The report had been delayed after the Securities and Exchange Commission raised questions about its cash flow statements in 2019 and 2020.

Last week, asset manager Harris Associates, Credit Suisse’s largest shareholder, completely exited its position in the bank, according to a Financial Times report. Credit Suisse declined to comment on the report.

This is the latest in a series of issues for the bank. The 170-year-old Swiss bank was hit hard by losses from the collapse of Archegos Capital and Greensill Capital in 2021. The bank has posted a loss for five straight quarters and is in the middle of its second major overhaul in as many years after a series of scandals, executive changes, and client withdrawals.

In November, Credit Suisse announced plans to spin out its investment bank under its revived First Boston brand. It also slashed 9,000 jobs.

Credit Suisse is now focusing on rebuilding its wealth management business. That unit experienced about $100 billion of outflows in the fourth quarter. Other than the Saudi National Bank, Credit Suisse’s biggest shareholders include Qatar Holding, Olayan Group, and BlackRock .

Shares of the bank are down 75% over the past year.

Credit Suisse Says It Will Borrow Up to $54 Billion From Swiss National Bank

Switzerland's regulators said Wednesday they will step in to help Credit Suisse if it becomes necessary to do so. Problems at the country's second-biggest lender caused stocks around the world to falter---and reignited fears for the banking sector.

www.barrons.com

www.barrons.com

No surprise at all (regarding what I wrote a few posts earlier especially)

hotair.com

hotair.com

Gavin Newsom had his handOUT for SVB bailOUT withOUT telling anyone he ( and 3 of his wineries) were clients?

Oh, how incestuous they are. It’s like the old Mafia saying with these progressive Democrats &

hotair.com

No surprise at all (regarding what I wrote a few posts earlier especially)

Gavin Newsom had his handOUT for SVB bailOUT withOUT telling anyone he ( and 3 of his wineries) were clients?

Oh, how incestuous they are. It’s like the old Mafia saying with these progressive Democrats &

Democrats are just as equally corrupt as the Republicans.

Crazy how they will point fingers at each other while in reality they work how they can beat each other.

Mehmed Ali

Contributor

")

Oh how charming, I was wondering for sometime, what would be the newest crisis " naturally and due to greed and stupidity " would be. Well , seemingly we are getting a bit of relief here. It is just simply usual " bank mismanagement ". Yet another step towards happiness. You know, before it gets better it will get a bit worse. Like every new thing, we are going through child birth troubles maybe. You will own nothing and be happy.

It is real good that system where the glorified Souk crooks , who some people call democracy, have chance to show us that the world is about them. I know I get it , for great new things you need the new proletariat. Proletariat of fat ugly pigs , homosexuals , minorities and the wronged people.

Hey at least when we go to the ballots, we have sense of the empowerment. As Henry Ford said " You can get any color as long as it's black".

It is real good that system where the glorified Souk crooks , who some people call democracy, have chance to show us that the world is about them. I know I get it , for great new things you need the new proletariat. Proletariat of fat ugly pigs , homosexuals , minorities and the wronged people.

Hey at least when we go to the ballots, we have sense of the empowerment. As Henry Ford said " You can get any color as long as it's black".

Democrats are just as equally corrupt as the Republicans.

Crazy how they will point fingers at each other while in reality they work how they can beat each other.

They definitely both have the same potential for corruption, they are all collective group of politicians after all.

But corruption realisation has been far greater on Democrat side overall in recent times especially (when you study the inner layers of it, which is a long subject so I wont bore folks with it all).

But in end it is literally why without any thinking at all..... they pushed through all this extra debt-laden spending under Biden that caused largest (layer 1) part of what is tipping over now.

Systematically this corruption basis scale is largely due to fact Democrats got and get their political power from the cities, especially inner cities.... (whereas Republicans now derive theirs from suburbs, towns and rural).

Cities are a real mishmash of corruption to begin with (all kind of issues get concentrated by sheer population density and jostling for wealth creation etc) and this gets worse when you have one party rule on top entrenched there...and then expand their bad habits federally (and internationally by extension).

This is specifically why Democrat party has abandoned all actual working class principle (it once espoused) and has turned into a marxist corporate intersectional alliance format.

It is simply what has been convenient (bad habits and consequences be damned) for them to retain status quo in the inner cities and try to expand into the suburb vote more.....by trying to pander to each "voter group", and plaster over the actual issues (like white liberal hypocrisy with NIMBYism, big money donors and racialised identity politics all at same time)....using the far larger institutional capture (and soft power side of it especially in media and hollywood etc) they got by expanding big govt (especially since LBJ).

All things that have thrown principle out the window (only liberal side can do this like it has)....whereas conservatives by their definition have to be rooted to some principle always (whether they individually do so past their identity is another subject).

In many ways the US would have been very different country now if Kennedy was not assassinated and had 2 full terms. He was really the last democrat that actually was balanced and cognisant to large degree on role of federal govt having to be restricted and focused on what its actually there for.

It would have prevented or been a huge obstacle to "big society" welfare at reckless federal level and Vietnam war (and the precedents these set for later use by big US federal govt, domestically and internationally)..... if the sympathy vote a total POS like LBJ got (and the power democrats got without much work for it in senate and house at that crucial time) never happened.

LBJ (by way of kennedy assassination) really was the root of so much corruption in the democrat party today (to add to what Wilson first really started with the Fed to begin with and then FDR started to grow even more during his tenure). The power for power sake concept that radical "progressives" of each era abuse.

There is a reason why Malcolm X said what he did about the white liberal. They will pretend to care (words), but actually are vicious hypocrites in the end (actions)....a wolf in sheep clothing I believe were his words. With conservatives, you at least know what you are getting right away and you can agree or disagree directly with it and move on to next thing from there....theres no BS.

It is whichever side that promotes more BS that creates the large space for worst forms of corruption (in every sense, socially and economically) to then fill into.

Last edited:

Mehmed Ali

Contributor

Ultimately, it is about just one thing , the absolute power. " Liberalism " in its nature has inherited weaknesses to create such thing unlike Communism. So by amalgam of few factors this people are trying, and so far succeeding, to create the absolute power. When the project is finished, there won't be any trace of " Liberal, progressive and left" idea or reality.

Communist China is in the reality National Socialist country almost in the purest form , Stalinist Russia was an extreme right wing in its nature. Ofcourse all that right wing was not what the real right wing should be about. Because the intentions, alliances created and the goals didn't have one single natural characteristic. It always appealed to the lowest instincts and desires. Though unnatural those things are , they are very strong. The Fatsos keep seeing themselves on Victoria Secrets adverts and getting resounding ovations from fellow cultists will never want to go back to old themselves. Ofcourse, they know in the majority of cases, how grotesque is all of that. So till something radical happens these schmucks will carry on. Another war , another financial chrisis another emergency another set of the oppressive laws etc.

Kennedy couldnt had carry on , especially after that famous speech in the Congress . Trump on some rally a few days ago , said something similar. I think both of them ( Trump and Kennedy) were too alone and isolated and that's the reason for their lack of success.

Communist China is in the reality National Socialist country almost in the purest form , Stalinist Russia was an extreme right wing in its nature. Ofcourse all that right wing was not what the real right wing should be about. Because the intentions, alliances created and the goals didn't have one single natural characteristic. It always appealed to the lowest instincts and desires. Though unnatural those things are , they are very strong. The Fatsos keep seeing themselves on Victoria Secrets adverts and getting resounding ovations from fellow cultists will never want to go back to old themselves. Ofcourse, they know in the majority of cases, how grotesque is all of that. So till something radical happens these schmucks will carry on. Another war , another financial chrisis another emergency another set of the oppressive laws etc.

Kennedy couldnt had carry on , especially after that famous speech in the Congress . Trump on some rally a few days ago , said something similar. I think both of them ( Trump and Kennedy) were too alone and isolated and that's the reason for their lack of success.

Last edited:

First Republic bank was on the edge. Now America’s largest banks are depositing $30 billion to try to save it

The latest multibillion effort to aid a bank is coming from the banking industry itself.A group of 11 banks has deposited $30 billion into First Republic, the California lender that many investors, analysts and depositors saw as teetering on the edge following the collapse of its similarly sized neighbor Silicon Valley Bank.

The banks’ plan was announced by Treasury Secretary Janet Yellen, Federal Deposit Insurance Corporation Chairman Martin Gruenberg and Acting Comptroller of the Currency Michael J. Hsu — and separately by the banks themselves. It was a coordinated show of force following the Sunday night announcement that all depositors of Silicon Valley Banks would be made whole and that the banking system would have access to special financing from the Federal Reserve.

While less dramatic than any type of direct federal support — there is no presidential press conference scheduled to discuss the deposits — the move by the banks shows that the banking system is still brittle following Silicon Valley Bank’s collapse and the Federal Reserve, FDIC and Treasury’s efforts to contain the fallout. This move was designed to further bolster the mid-size banking sector, which has seen a decline in deposits in favor of the largest banks, which are often perceived as safer for depositors.

It’s also a sign that First Republic’s efforts to distinguish itself from Silicon Valley Bank were only so successful. While the $30 billion in deposits is a sign that the banks had faith in the survival of First Republic, it also shows that potential deposit outflows — caused by concerns that the bank’s largely wealthy depositor base could see their money disappear if the bank were to fail — are still a concern for the industry.

The Federal Reserve also announced that banks had borrowed over $160 billion from the central bank’s emergency lending programs, indicating that the need for financing goes beyond a few obviously troubled banks.

Reversing the flow

While the deposits do not guarantee First Republic’s continued health, they do show that the banking industry — including the megabanks — is concerned about the flow of deposits from mid-size and smaller banks into larger ones, which could put those mid-size banks at risk of failure.That First Republic needed the deposits at all shows the limits of the FDIC and Treasury’s guarantee of Silicon Valley Bank and Signature Bank depositors. While many interpreted the deposit guarantee as implicitly backing the deposits of the entire banking system, the massive infusion Thursday to counter deposit outflows shows that many bank depositors are still worried about even large mid-size banks.

The largest banks in the country participated in the effort, including JPMorgan Chase, Bank of America, Citigroup and Wells Fargo, who deposited $5 billion each.

The banks framed the mass deposit as part of an effort to counteract and perhaps even prevent further deposit withdrawals at “a small number of banks.” Overall, the banks said, “The banking system has strong credit, plenty of liquidity, strong capital and strong profitability. Recent events did nothing to change this. … Together, we are deploying our financial strength and liquidity into the larger system, where it is needed the most.”

First Republic’s attempts to stand out

At the end of last year, First Republic had around $212 billion of assets, making it the 14th-largest bank in the country — putting it just north of Silicon Valley Bank, the 16th-largest bank before it collapsed. If First Republic had failed, it would have been the second-largest bank failure in American history, supplanting Silicon Valley Bank.First Republic shares closed up 10 percent Thursday, perhaps indicating that the acute danger of its collapse had passed. As worries mounted following Silicon Valley Bank’s failure, First Republic spent much of the last week trying to differentiate itself, despite some considerable similarities.

In its most recent financial report, the bank said it had $176 billion of deposits, with almost $120 billion not insured by the Federal Deposit Insurance Corporation. This fact alone was enough to put a target on the bank’s back, as it was comparable to Silicon Valley Bank’s ratio of uninsured deposits. The bank also said in its annual report that over 90 percent of its funding comes from deposits, which means if the bank failed, its overall losses would not have to be that high in order to hit its uninsured depositors.

In recent days, First Republic has tried to stress how different it is from Silicon Valley Bank, pointing out that only 9 percent of its deposits come from any one sector, in contrast to SVB’s reliance on technology and life sciences. What First Republic was trying to demonstrate was that it wasn’t at risk of a group-chat-driven bank run where a highly networked group of investors and executives all decided to try to take all their money out at the same time.

Similar risks and trickier politics

But industry analysts weren’t so sure the distinctions First Republic tried to draw were more important than the similarities. In a note explaining why it declared First Republic’s debt to be riskier, the ratings agency Fitch said that First Republic’s deposit base was still “concentrated” and that because of the bank’s “strategic focus on banking wealthy and financially sophisticated customers in select urban coastal markets in the U.S.,” there was both a high percent of uninsured deposits and that those deposits could be “less sticky in times of crisis or severe stress.” In other words, even if they came from different industries, the bank’s depositors were still wealthy individuals and businesses concentrated on the coasts that could potentially move at the same time to withdraw their money if they were worried they weren’t getting it back.While Silicon Valley Bank provided high levels of customer service and personal banking to technology founders and investors as part of its overall strategy to serve technology businesses, First Republic “has a uniquely focused business model, with a high service offering aimed at wealthy clients concentrated in coastal urban areas,” Morningstar analyst Eric Compton wrote in a February research report. The bank also specialized in real estate lending to those wealthy costal elites, including a mortgage for Mark Zuckerberg.

The bank’s focus on high-end customers could have made any explicit government support politically tricky. The rescue of Silicon Valley Bank depositors is already controversial, even as the company had many corporate and even nonprofit customers who relied on it for payroll. First Republic’s depositors may have been less sympathetic.

But like Silicon Valley Bank, First Republic was also reporting substantial losses on its portfolio of bonds, although not as severely as Silicon Valley Bank before its collapse. “If it were to face higher-than-anticipated deposit outflows and liquidity backstops proved insufficient, the bank could need to sell assets, thus crystalizing unrealized losses,” the rating agency Moody’s said Monday.

Since Silicon Valley Bank’s collapse, First Republic has tried to reassure shareholders in clients, saying in a press release on Friday that its “deposit base is strong and very-well diversified,” its “liquidity position remains very strong” (i.e., it could handle deposit withdrawals) and that it was well capitalized. On Monday, it sought to reassure clients, depositors and investors again, announcing that it had “diversified its financial position through access to additional liquidity from the Federal Reserve Bank and JPMorgan Chase.”

This was an attempt to show that the central bank and the nation’s largest bank still saw it as a bank safe enough to lend to. The bank also made use of a special lending facility set up by the Federal Reserve. The shares still went down violently on Monday and rose again on Tuesday before falling again on Wednesday. From the close of trading last Thursday through Wednesday, the bank’s share prices had fallen by two-thirds.

Like its “mid-size” peers, First Republic will likely have to undergo more scrutiny in the wake of the collapse of Silicon Valley bank, which could further dent profits, Compton wrote in a note earlier his week.

First Republic bank was on the edge. Now America’s largest banks are depositing $30 billion to try to save it

The latest multibillion effort to aid a bank is coming from the banking industry itself. A group of 11 banks has deposited $30 billion into First Republic, the California lender that many investors, analysts and depositors saw as teetering on the edge following the collapse of its similarly...

Exclusive: Credit Suisse to hold internal talks this weekend on scenarios for bank -sources

Credit Suisse AG (CSGN.S) will hold meetings over the weekend to assess scenarios for the bank as it struggles to regain the market's confidence, people with knowledge of the matter told Reuters on Friday.The meetings will involve teams reporting to Chief Financial Officer Dixit Joshi, the people said. Executives will run through the numbers and formulate scenarios that might reshape Credit Suisse's future, the sources added.

Credit Suisse declined to comment.

On Thursday, the bank said it would seek a $54 billion loan from the Swiss National Bank after its customers pulled more than $100 billion in funds in recent months and its shares plunged 25% on Wednesday.

The emergency lifeline has provided the embattled lender with some relief but its shares resumed their descent on Friday.

With investor confidence still weak, some analysts have said the loan facility has only bought Credit Suisse time to work out what to do next strategically to restore profitability.

Among possible scenarios, analysts, bankers and investors speculate that Credit Suisse could sell or wind down some of its existing businesses with a break-up potentially on the cards.

A more decisive solution could be an outright takeover by a rival.

A string of scandals over many years, top management changes, multi-billion dollar losses and an uninspiring turnaround strategy can be blamed for the troubles that the 167-year-old Swiss lender finds itself in.

The sell-off in Credit Suisse's shares began in 2021, triggered by losses associated with the collapse of investment fund Archegos and Greensill Capital.

In July, new CEO and restructuring expert Ulrich Koerner unveiled a strategic review that failed to win over investors.

An unsubstantiated rumour on an impending failure of the bank in the autumn sent customers fleeing.

Credit Suisse confirmed last month that clients had pulled 110 billion Swiss francs of funds in the fourth quarter while the bank suffered its biggest annual loss of 7.29 billion Swiss francs since the financial crisis. In December, Credit Suisse had tapped investors for 4 billion Swiss francs.

On Wednesday, Saudi National Bank (1180.SE), the bank's top backer, told reporters it could not give more money to the bank as it was constrained by regulatory hurdles, though it was supportive of the bank's turnaround plan.

Exclusive: Credit Suisse to hold internal talks this weekend on scenarios for bank -sources

Credit Suisse AG will hold meetings over the weekend to assess scenarios for the bank as it struggles to regain the market's confidence, people with knowledge of the matter told Reuters on Friday.

SVB execs sold millions of their company stock in lead up to collapse, federal disclosures show

Less than two weeks before Silicon Valley Bank became the largest bank failure since the 2008 financial crisis, top executives at the company sold stock totaling several million dollars, according to federal disclosures obtained by ABC News.

Former SVB President and CEO Greg Becker sold over $3.5 million of his company stock holdings on Feb. 27, according to a disclosure made to the U.S. Securities and Exchange Commission filed on March 1.

Becker wasn't the only member of SVB's top brass to sell company common stocks. In a separate FEC disclosure, also filed March 1, SVB Chief Financial Officer Daniel Beck sold $575,180 in company common stocks on Feb. 27.

ABC News reported this week that the Justice Department and Securities and Exchange Commission are probing the collapse of Silicon Valley Bank, according to two people familiar with the situation.

The probes, which are separate, are in the preliminary stages and it is not clear whether any wrongdoing has been committed. It is not unusual after a large public collapse of a bank or company for the Justice Department or SEC to step in and investigate.

Sources are telling ABC News that part of the FBI's early focus will be looking into whether any of Silicon Valley's senior leadership got unusual bonuses or sold stocks in the days leading up to the bank's collapse. In short–is there any evidence of insider trading.

The U.S. Justice Department and SEC both declined ABC News' requests for comment.

In the days following Becker's sale of millions of dollars in his SVB shares and before the bank's collapse, the then-CEO appeared confident during remarks to an audience of investors, Wall Street analysts and technology executives attending a technology conference in San Francisco's Palace Hotel, according to a copy of his remarks obtained by ABC News.

One day after Becker's reported remarks, SVB announced a $1.8 billion loss on the sale of securities, including Treasury and mortgage bonds which had lost significant value over the previous year due to an aggressive series of interest rate hikes at the Federal Reserve. The bank laid out plans to raise more than $2 billion in an effort to shore up its balance sheet.

According to the New York Times, the week before Becker's confident projection at the tech conference – and then the bank's ultimate collapse – the rating agency Moody's had called to tell Becker "the banks bonds were in danger of being downgraded to junk." That would mean the call came around the same time Becker sold the over $3.5 million of his SVB common stock on Feb 27.

Asked by ABC News to confirm the call, a spokesperson for Moody's declined to comment.

Becker did not respond to multiple requests from ABC News for comment. Silicon Valley Bank spokespeople directed queries from ABC News to the Federal Deposit Insurance Corporation.

In the bank's SEC annual report for the end of 2022, filed on Feb. 24, under "Credit Risks," the company wrote, "Because of the credit profile of our loan portfolio, our levels of nonperforming assets and charge-offs can be volatile. We have and may in the future need to make material provisions for credit losses in any period, which could reduce net income, increase net losses or otherwise adversely affect our financial condition in that period. Our loan portfolio has a credit profile different from that of most other banking companies. The credit profiles of our clients vary across our loan portfolio, based on the nature of our lending to different market segments.

Another risk factor, the company disclosed, was that their "interest rate spread may further decline in the future. Any material reduction in our interest rate spread could have a material adverse effect on our business, results of operations or financial condition."

Under the subsection for "Legal, Compliance and Regulatory Risks," SVB said the same regulations now deemed to have been not strong enough were so cumbersome that they could risk business at the company.

"We are subject to extensive regulation that could limit or restrict our activities, impose financial requirements or limitations on the conduct of our business, or result in higher costs to us, and the stringency of the regulatory framework applicable to us may increase if, and as, our balance sheet continues to grow," SVB wrote in its annual filing.

"As a bank holding company with more than $100 billion of average total consolidated assets, we are subject to stringent regulations, including certain enhanced prudential standards applicable to large bank holding companies. If we exceed certain other thresholds, we will become subject to even more stringent regulations," it added.

SVB execs sold millions of their company stock in lead up to collapse, federal disclosures show

Former SVB President and CEO Greg Becker sold over $3.5 million of his company stock holdings on Feb. 27, according to a disclosure made to the SEC.

UBS to Buy Credit Suisse in $3.25 Billion Deal to End Crisis

- Government to backstop some losses, provide liquidity

- Authorities pushed for deal amid worsening confidence crisis

UBS Group AG agreed to buy Credit Suisse Group AG in a historic, government-brokered deal aimed at containing a crisis of confidence that had started to spread across global financial markets.

The Swiss bank is paying 3 billion francs ($3.25 billion) for its rival in an all-share deal that includes extensive government guarantees and liquidity provisions. The price is less than half the 7.4 billion francs Credit Suisse was worth at the close of trading on Friday.

The Swiss National Bank is offering a 100 billion-franc liquidity assistance to UBS while the government is granting a 9 billion-franc guarantee for potential losses from assets UBS is taking over. Regulator Finma said about 16 billion francs of Credit Suisse bonds will become worthless to ensure private investors help shoulder the costs.

The plan, negotiated in hastily arranged crisis talks over the weekend, seeks to address client outflows and a massive rout in Credit Suisse’s stock and bonds over the past week following the collapse of smaller US lenders. A liquidity backstop by the Swiss central bank mid-week failed to end a market drama that threatened to send counterparties fleeing, with potential ramifications for the broader industry.

“It was indispensable that we acted quickly and find a solution as quickly as possible“ given that Credit Suisse is a systemically important bank, Swiss National Bank President Thomas Jordan said at a press conference late Sunday.

US authorities had been working with their Swiss counterparts because both lenders have operations in the US and are considered systemically important in Switzerland, Bloomberg reported earlier. Authorities sought an agreement before markets opened again in Asia.

UBS Chairman Colm Kelleher said he will shrink Credit Suisse’s investment bank, a unit that has racked up losses in recent years, while he’s determined to keep the Swiss universal bank, the one business of Credit Suisse that remained a relative bastion of stability in the crisis.

“Let me be very specific on this: UBS intends to downsize Credit Suisse’s investment banking business and align it with our conservative risk culture,” he said at a press conference announcing the deal.

The takeover of the 166 year-old lender marks a historic event for the nation and global finance. The former Schweizerische Kreditanstalt was founded by industrialist Alfred Escher in 1856 to finance the build-out of the mountainous nation’s railway network. It had grown into global powerhouse symbolizing Switzerland’s role as a global financial center, before struggling to adapt to a changed banking landscape after the financial crisis.

UBS traces its roots back through some 370 separate institutions over 160 years, culminating in the merger of the Union Bank of Switzerland and the Swiss Bank Corporation in 1998. After emerging from a state bailout during the 2008 financial crisis, UBS built a reputation as one of the world’s largest wealth managers, catering to high- and ultra-high net worth individuals globally.

While Credit Suisse avoided a bailout during the financial crisis, it has been hammered over recent years by a series of blowups, scandals, leadership changes and legal issues. Clients had pulled more than $100 billion of assets in the last three months of last year as concerns mounted about its financial health, and the outflows continued even after it tapped shareholders in a 4 billion-franc capital raise.

Silicon Valley Bank UK arm hands out £15m in bonuses days after £1 rescue

Between £15m and £20m in bonus payments were made to staff at SVB UK this week after being signed off by the bank's new owner, HSBC, Sky News learns.

The British arm of Silicon Valley Bank (SVB UK) has handed out millions of pounds in employee bonuses just days after its insolvency was averted through a Bank of England-orchestrated rescue deal.

Sky News has learnt that the payouts to staff including its senior executives were signed off by HSBC, SVB UK's new owner, earlier this week.

Sources described the bonus pool as "modest", and said it totalled between £15m and £20m.

It was unclear on Saturday how much had been awarded to Erin Platts, the UK bank's chief executive or her senior colleagues.

One insider said the bonus payments were a signal of HSBC's confidence in the talent base at its new subsidiary and that the buyer had been keen to honour previously agreed payments in order to help retain key staff.

Employing about 700 people in Britain, SVB UK is a profitable business but was brought to the brink of collapse last weekend by the travails of its American parent company.

Had it not been acquired solvently, the bonuses would not have been paid this week, according to insiders.

One pointed out that stock held by senior executives and other employees had been rendered worthless by SVB UK's near-collapse.

In the US, its banking arm has been taken into government ownership and its holding company, SVB Financial Group, has now filed for Chapter 11 bankruptcy protection as it seeks buyers for its other assets.

Bonuses were also paid to its US staff just hours before the Santa Clara-based bank collapsed, according to reports last week.

An emergency auction in which Rishi Sunak, the prime minister, played a pivotal role drew interest from challenger banks including Oaknorth and The Bank of London.

HSBC, Europe's biggest lender, struck a deal before markets opened in London on Monday to buy SVB UK for £1.

It was given a waiver from bank ring-fencing rules introduced after the 2008 financial crisis.

Jeremy Hunt, the chancellor, said the rescue had been critical to preserving funding to some of the UK's most promising start-up companies.

"The UK's tech sector is genuinely world-leading and of huge importance to the British economy, supporting hundreds of thousands of jobs," he said.

"We have worked urgently to deliver on that promise and find a solution that will provide SVB UK's customers with confidence.

"[This] ensures customer deposits are protected and can bank as normal, with no taxpayer support."

The government had been lobbied intensively last weekend by hundreds of tech entrepreneurs about the parlous state of SVB UK.

They warned of "an existential threat to the UK tech sector", adding: "The Bank of England's assessment that SVB going into administration would have limited impact on the UK economy displays a dangerous lack of understanding of the sector and the role it plays in the wider economy, both today and in the future."

The founders warned Mr Hunt that the collapse of SVB UK would "cripple the sector and set the ecosystem back 20 years".

"Many businesses will be sent into involuntary liquidation overnight," they wrote.

Sky News revealed this week that Ms Platts, who has worked in the lender's British operations since 2007, would remain in her job following talks with Ian Stuart, the HSBC UK chief executive.

SVB UK's independent directors, who include chairman Darren Pope, are also expected to stay on under HSBC's ownership.

That indicates HSBC's intention to enable the technology-focused lender to operate with some degree of autonomy on an ongoing basis.

However, the Silicon Valley Bank brand may disappear in the UK, depending upon its fate in the US, one insider said.

The turmoil at SVB has threatened to escalate into a much broader banking crisis, with the Financial Times reporting on Friday evening that UBS is in talks to take over part or all of its Zurich-based peer, Credit Suisse.

In the US, a group of large lenders including Bank of American and JP Morgan provided a $30bn deposit lifeline to First Republic on Thursday.

However, its shares continued to slump on Friday, raising renewed fears for its health.

A spokesman for SVB UK declined to comment on the bonus payments handed out this week.

Silicon Valley Bank UK arm hands out £15m in bonuses days after £1 rescue

Between £15m and £20m in bonus payments were made to staff at SVB UK this week after being signed off by the bank's new owner, HSBC, Sky News learns.

Banking crisis threat to energy markets?

Just as the energy crisis appears to be easing in Europe in 2023, a potential banking crisis ignited last week.

This was initially sparked in the US with the collapse of two mid-tier banks (Silicon Valley & Signature). But contagion quickly spread to Europe with solvency concerns resurfacing over some large European banks e.g. Credit Suisse & Deutsche Bank.

The threat of a banking crisis triggered a strong market reaction with falling commodity prices and one of the sharpest ever declines in global interest rates, as markets priced in an increasing risk of a sharp economic contraction.

It has been a while since we stepped back and looked at the macro factors impacting energy markets. So in today’s article we take a 5 chart tour of some key macro drivers in play and their implications for energy markets.

1. Bank risk

The banking sector is not our area of expertise, but it is useful to start with some quick factual context on current market events.Banking stress emerged two weeks ago with a ‘deposit run’ on mid-size US banks. Depositors withdrew cash in a flight to safety, moving into larger banks or government securities (which also offered higher returns). The US Federal Reserve has been forced to make large liquidity injections into the banking system in an attempt to stem contagion.

Stress then spread to European banks. Credit Suisse in particular suffered a sharp fall in its share price given growing solvency concerns. This was not helped by its largest shareholder (Saudi National Bank) stating it will not inject more capital to prop up the bank.

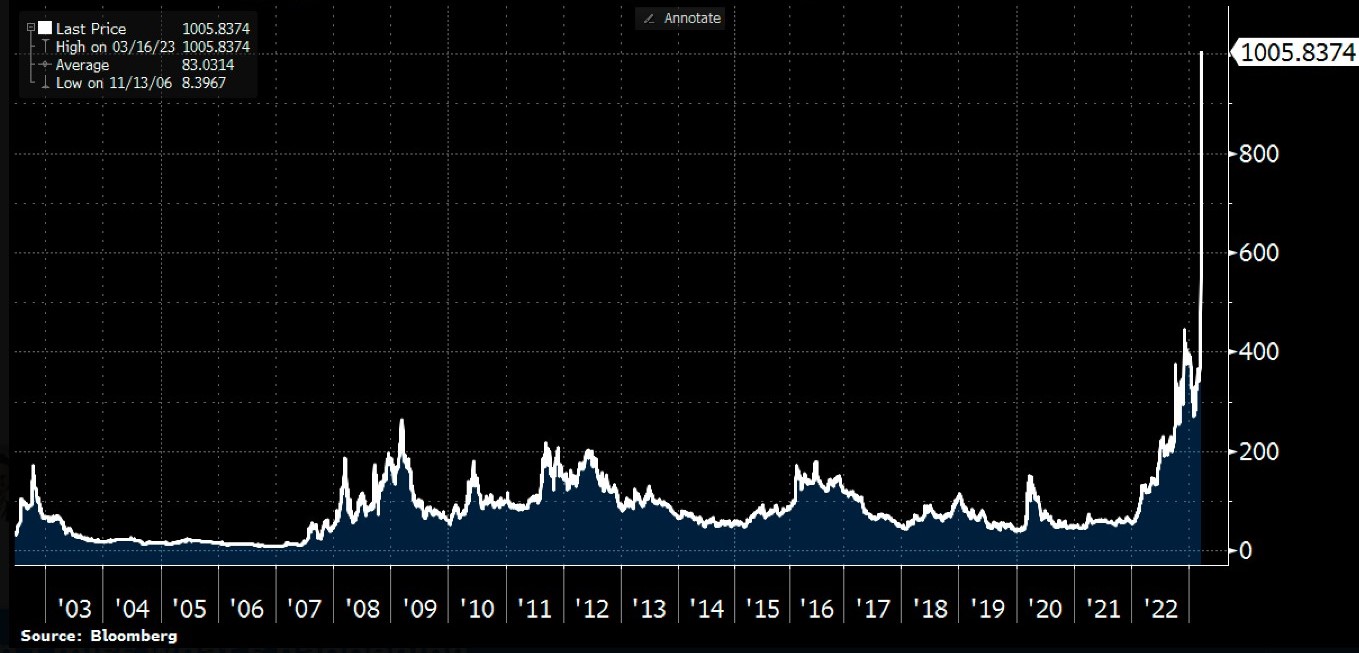

The Swiss central bank stepped in to provide Credit Suisse with liquidity support but despite this default risk soared. Chart 1 shows market pricing of insurance against Credit Suisse default surging exponentially late last week.

To stave off a disorderly collapse, Switzerland’s largest bank UBS agreed to buy Credit Suisse on Sunday afternoon in what was effectively a forced takeover that wiped out a substantial portion of remaining equity value.

Chart 1: Credit Default Swap cost of insuring against Credit Suisse default

Importantly, other large European banks also saw sharp declines in share prices last week given contagion fears, with Deutsche Bank a particular concern.

From an energy market perspective the policy response to banking stress may have a bigger impact than the banking issues themselves. In order to explore the policy response it helps to take a look at two key macro drivers: inflation & interest rates.

2. European inflation

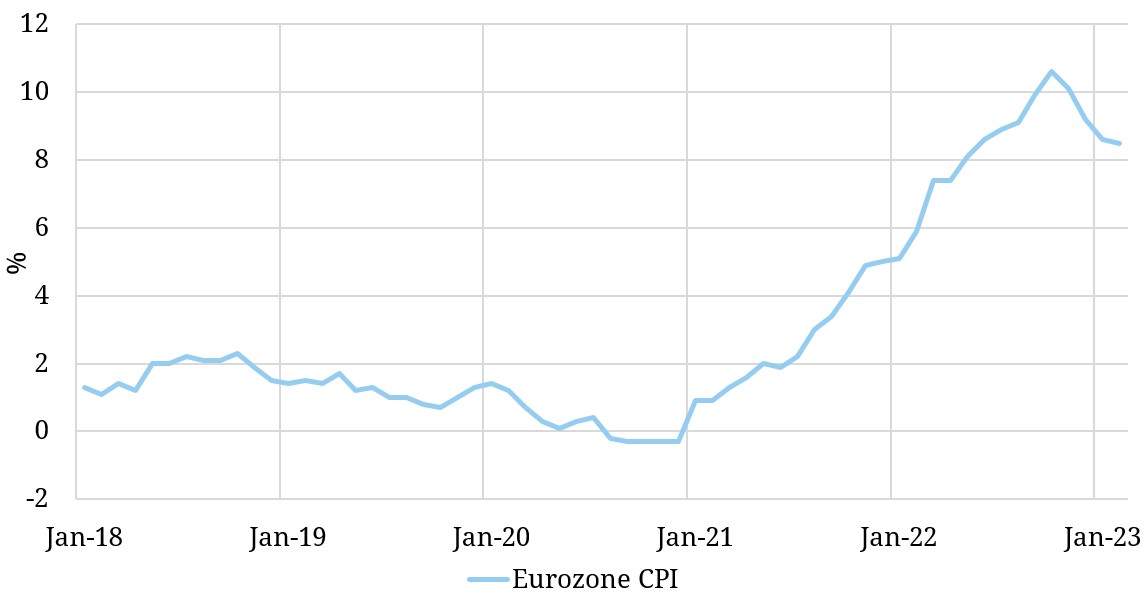

Inflation has been the dominant driver of both fiscal (government) and monetary (central bank) policy across 2022. Gas & power prices have been a key factor driving Eurozone inflation.Chart 2 shows the surge in Eurozone consumer price inflation (CPI) across 2021 & 2022 after years of relatively low and stable levels.

Chart 2: Eurozone inflation

Although inflation has eased slightly in 2023 it remains at elevated levels versus the 2% European Central Bank (ECB) inflation target.

Until the recent bout of banking stress hit, the ECB was firmly focused on tightening monetary policy (e.g. via interest rate hikes). However the threat of a banking crisis trumps inflation concerns, at least temporarily.

Banking stress may force central banks and governments into changing policy direction to prevent contagion. That was reflected in some very big moves in interest rates last week.

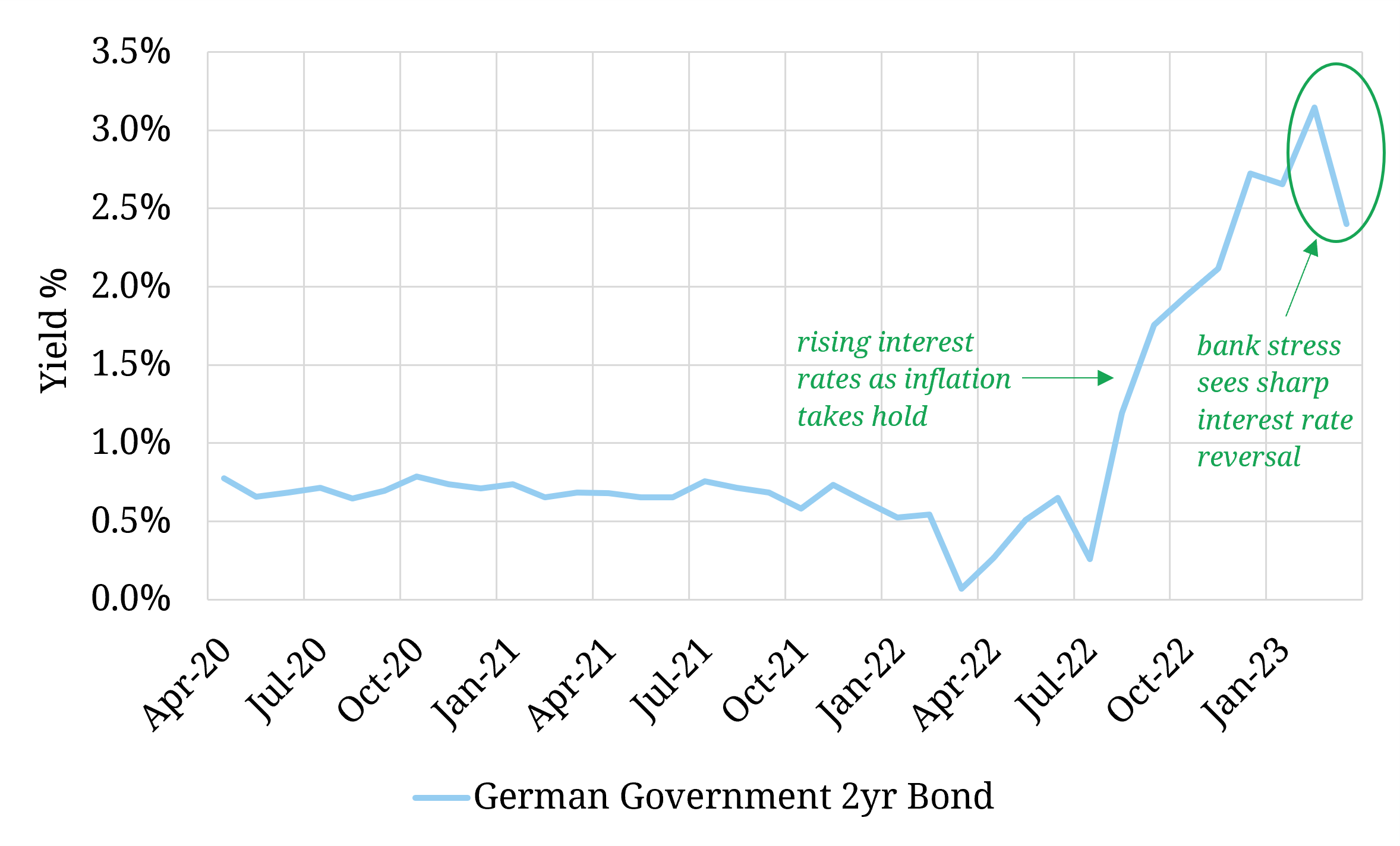

3. European interest rates

European interest rates surged in 2022 as inflation took hold and the ECB started hiking rates. Chart 3 shows a big move higher in German 2-year interest rates since Q3 2022. That is until last week when rates rapidly reversed course in response to bank stress.German 2 year rates fell from 3.3% to 2.4% over the course of a week, mirrored by similar moves across other European countries. This was one of the sharpest interest rate moves for decades and signals the emergence of a major economic threat.

Chart 3: German 2-year interest rates

The sharp decline in interest rates last week was a global not just a European event. It reflects markets pricing in a potential shift in central bank policy due to:

- a need to back off rate hikes (& potentially cut aggressively) in order to contain banking stress

- rising risk to economic growth as a result of a rapid contraction in bank lending.

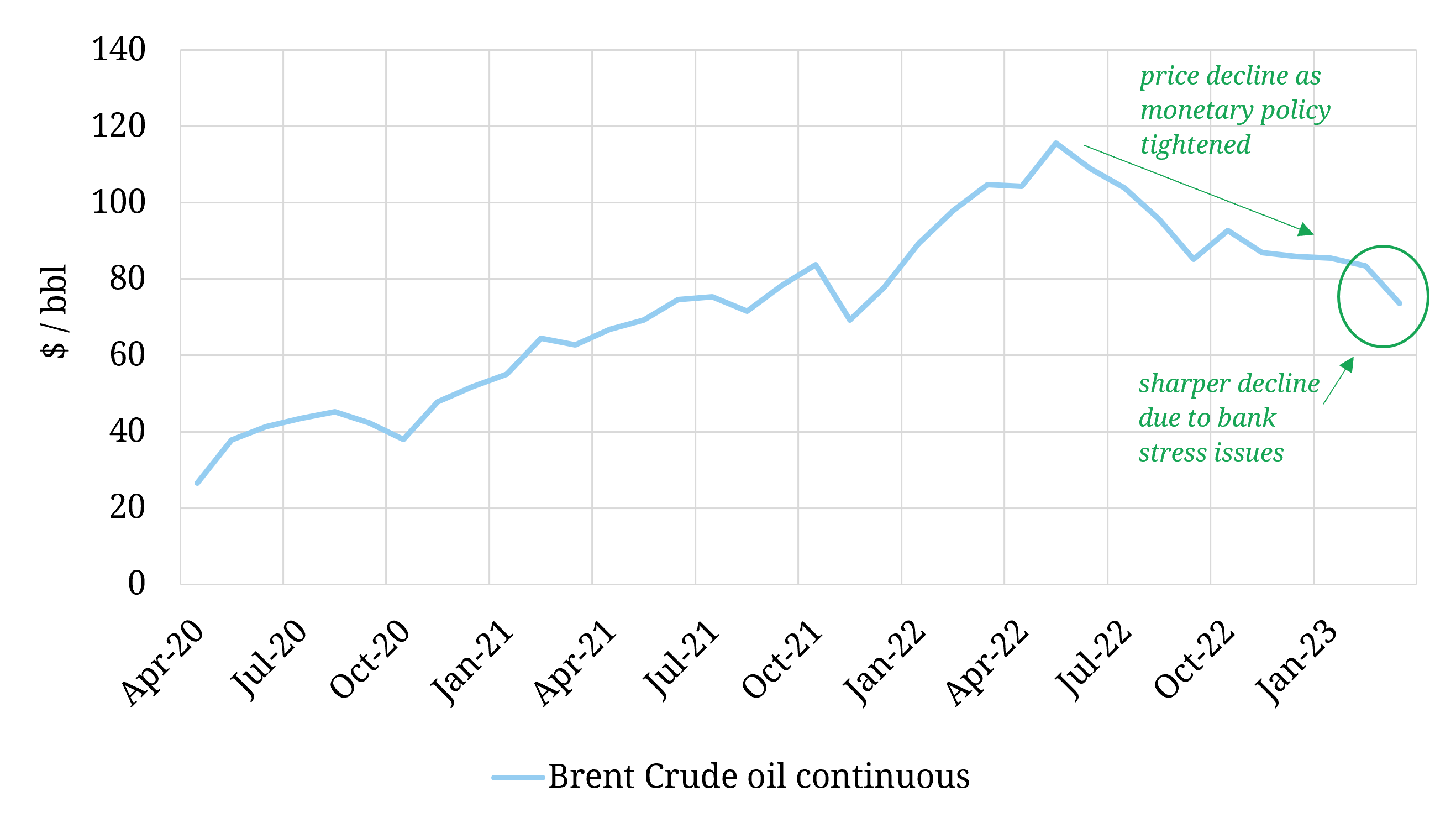

4. Commodity prices

Economic growth is closely linked to commodity demand. Banking stress has been reflected in commodity price movements over the last two weeks, e.g. across oil, gas, carbon & metals prices.Chart 4 shows the decline in Brent crude prices from around 85 $/bbl two weeks ago to 72 $/bbl last Fri.

Chart 4: Brent crude front month contract price

European energy markets have been dominated by specific supply & demand balance issues relating to the energy crisis across 2021-22. But macro drivers are becoming more important again in 2023 as the crisis has eased.

European gas & power markets have once again become re-anchored to coal for gas plant switching levels, with oil for gas switching also playing a role in setting Asian & European gas prices. As global commodity prices reassert their influence on European energy markets, there is on one more key macro driver worth looking at.

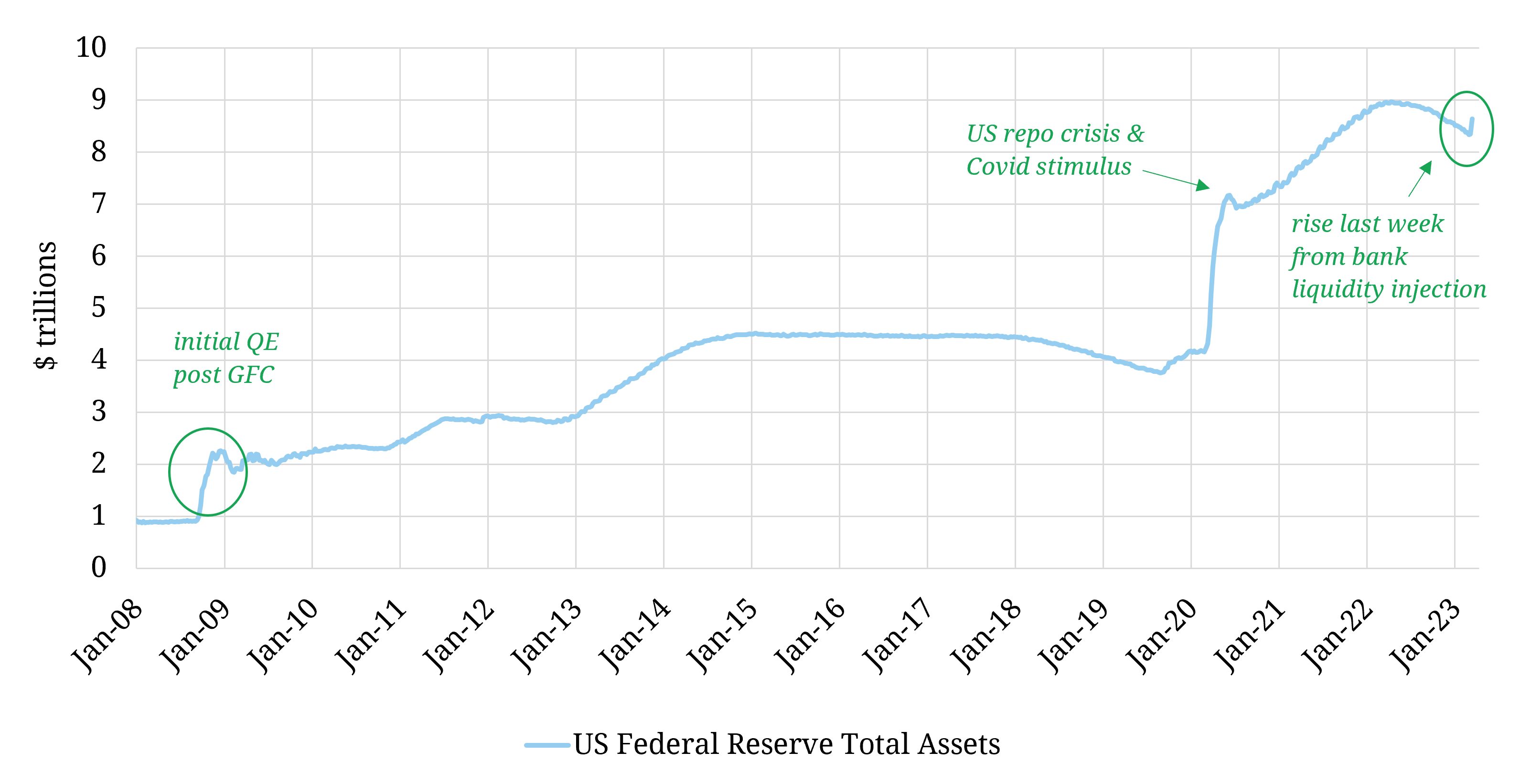

5.Central bank balance sheets

It is very unlikely that current banking stress turns into a 2008 style banking crisis. Governments and central banks have a much better prepared set of policy response tools. But the nature of the policy response may have important implications for energy & other commodity markets.Central banks are likely to fight a banking crisis with some form of monetary easing e.g. quantitative easing (QE) and balance sheet expansion (as they have done in the past).

Chart 5 shows the size of the US central bank (Fed) balance sheet. The broad trends here are reflective of the ECB and Bank of England balance sheets which have undertaken similar QE programs.

Central bank balance sheets contracted across 2022 after a long period of expansion, as central banks raised rates and wound down QE in an attempt to fight inflation. That has contributed to commodity price declines across the last 6 to 9 months.

There was a clear inflection in the Fed balance sheet last week (a $300 bn surge) as it was forced to inject liquidity into the banking system.

Chart 5: US Federal Reserve balance sheet assets

The scale of central bank response required to contain banking stress will be a key factor to watch across the next few weeks. There are two time horizons in play.

In the near term, the more that banking contagion spreads, the greater the risk of contraction in bank lending & economic growth. That will likely weigh on commodity & energy prices.

But if the threat of a banking crisis forces central banks to back off rate hikes and resume Quantitative Easing, it may provide more structural tailwinds again for global commodity prices as the dust settles, as we saw after the Covid demand shock in 2020.