Indonesia e-wallet transaction to reach $18.5 billion in 2021 amid fierce competition

5 min read

By

Janine Marie Crisanto

As the number of e-wallet players in Indonesia surges amid the vast market opportunities, bigger players have begun extending the competition beyond payments

- Local fintech players are currently dominating Indonesia’s digital payments space

- Bank and non-bank players are collaborating to amass scale in the midst of competition

- Indonesian e-wallet players are looking beyond payments to expand their ecosystems and create a bigger economic impact

Indonesia has always been ripe for digital disruption in financial services. The country has a huge population of 270 million and more than 50% are still unbanked due to geographical and infrastructural barriers. Nevertheless, Indonesia is one of the leading countries in the region in terms of internet and mobile penetration with over 60% of the population equipped with a smartphone according to a Google study.

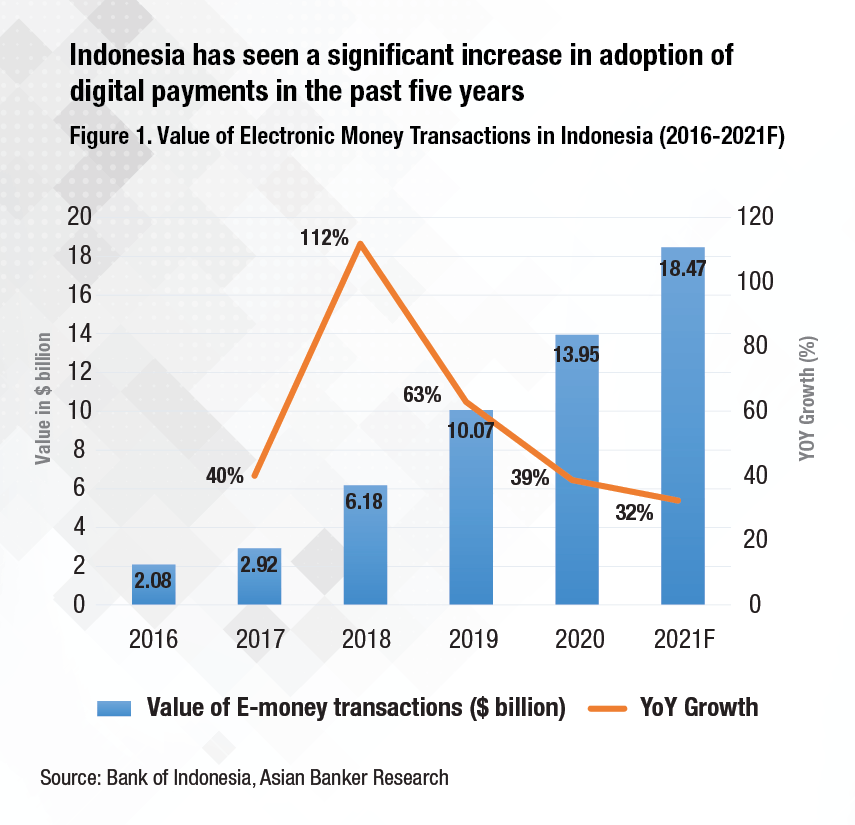

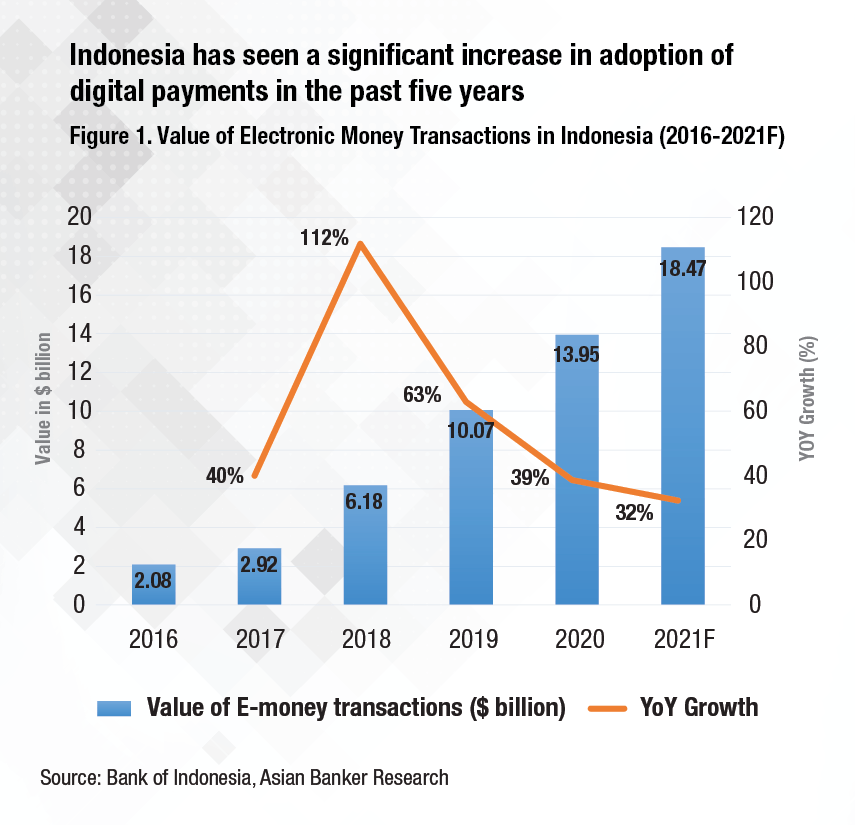

In the face of restrictions and lockdowns brought about by the COVID-19 pandemic, Indonesia has seen a surge in digital adoption among consumers and an accelerated growth of both digital payments and e-commerce platforms. According to Bank Indonesia (BI), the value of electronic money transactions reached IDR 201 trillion ($13.95 billion) in 2020, growing by 38.62% from IDR 145 trillion ($10.07 billion) in 2019. As of January 2020, the largest driver of digital transactions is retail at 28%, followed by transportation (27%), food order (20%), e-commerce (15%), and bill payments (7%).

The rising digital payments transactions reflect the evolving digital financial literacy of the Indonesian population. It also demonstrates the increasing acceptance of fintech and e-commerce services in the country. BI foresees that the uptake of digital transactions will continue with e-commerce and e-payments growing by 33.2% and 32.3%, respectively in 2021.

Local e-wallet players are currently dominating Indonesia’s digital payments space

With this opportunity, the industry has seen an influx of e-wallet providers in the past years. Currently, the digital payments landscape in Indonesia has become fiercer and more fragmented with more than 48 licensed e-wallet platforms led by domestic players from both public and private sectors.

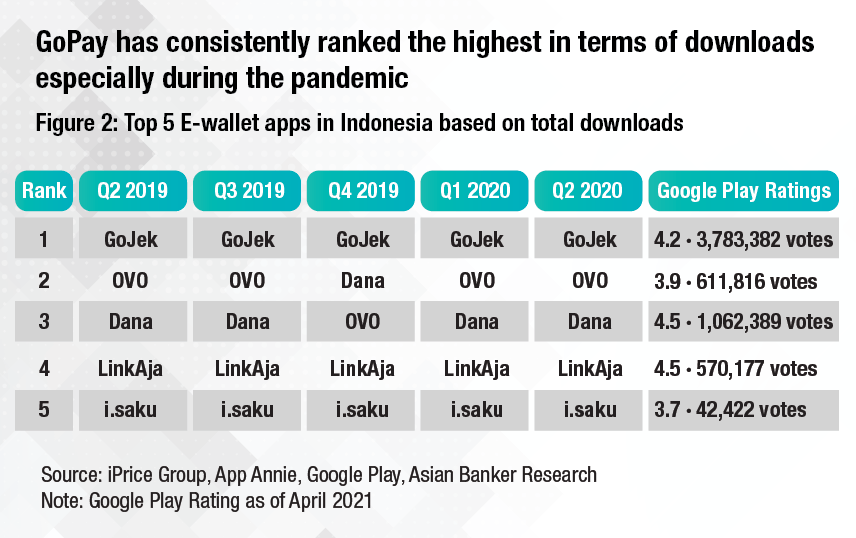

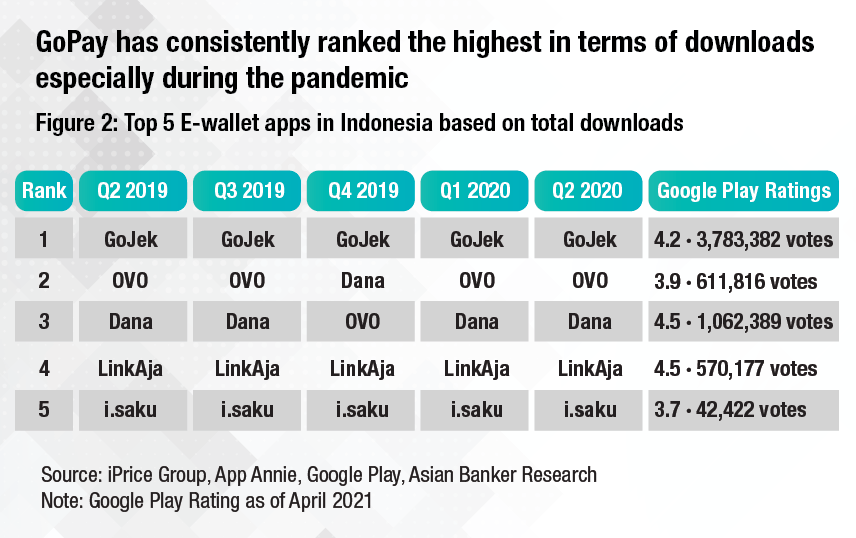

In this saturated market, scale and customer experience are key competitive advantages and differentiators for e-wallet providers. According to a recent study by iPrice and App Annie, GoPay and OVO are the top two e-wallets with the highest number of active monthly users and are the top apps with the most downloads during the Q2 2019-Q2 2020 period. However, in terms of customer reviews on the Google Play, Dana and LinkAja received the highest rating of 4.5 stars.

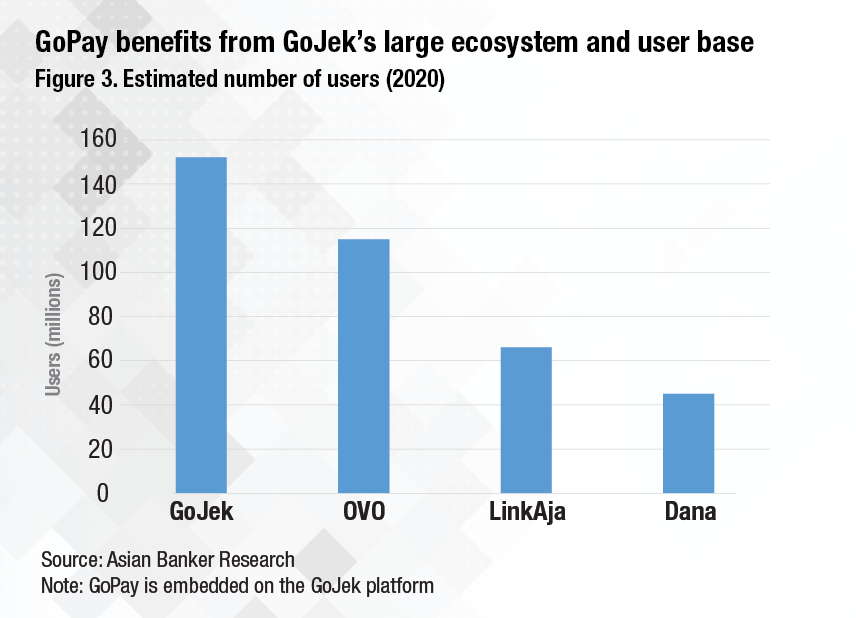

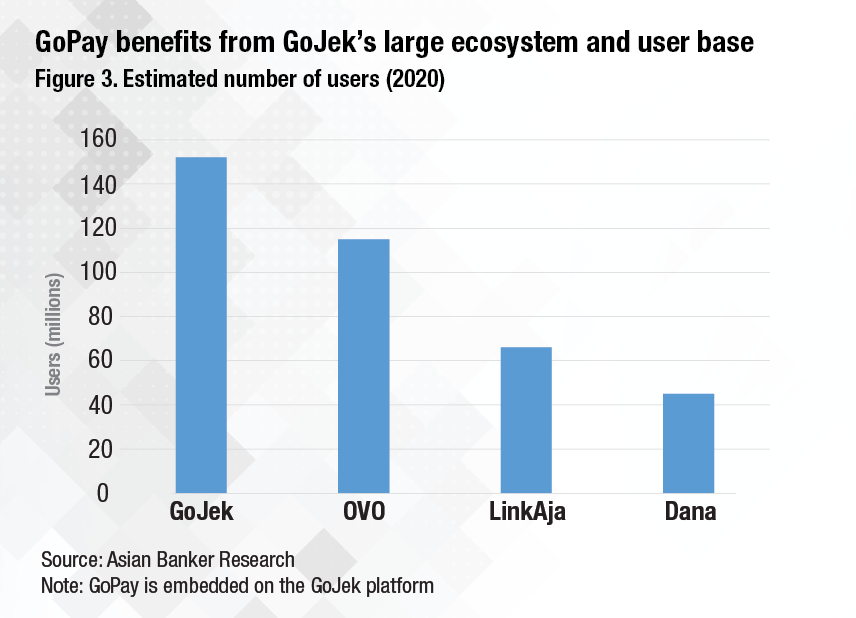

GoPay and OVO, both launched in 2016, have an advantage as they are backed by super-apps. GoPay is embedded as a payment service in Gojek which is the largest multi-service platform in the country. Meanwhile, OVO has grown over the years driven by its collaboration with the regional ride-hailing services Grab and Indonesia’s online e-commerce market Tokopedia. Dana, introduced in 2017, also leverages its linkages with the Indonesian media conglomerate Emtek Group and e-commerce marketplace Bukalapak. Dana is also backed by Alibaba.

Hans Patuwo, head of payments of Gojek Group, said, “The pandemic has accelerated the trend towards digital services as more people practice physical distancing and look online to meet daily needs. During this period we observed a growing reliance on cashless payments especially for bill payments, e-commerce and investments with last year’s gross transaction value for our payments-related businesses exceeding pre-pandemic levels”.

Jason Thompson, CEO of OVO, claimed the shift in

contactless transactions in the past years and the Indonesian government's active support to e-payments have greatly benefited its platform. “After the onset of COVID-19 we saw a 267% increase in new users. Subsequently we saw a rise in new merchants joining the OVO platform especially micro, small, and medium enterprises (MSMEs). The number of MSMEs on the OVO platform grew by 95.0% during 2020 with acceleration in the second half. This is an indication that MSMEs are seeing real benefits to their businesses from digital.”

Bank and non-bank players are collaborating to amass scale

Bank and non-bank players are collaborating to amass scale

Meanwhile, banks have also positioned themselves amid the increasing payments competition by introducing a government-owned e-wallet platform in June 2019 – LinkAja. The integrated payments platform is already at an advantage as it leverages the synergy and existing user base of its bank owners, namely Bank Mandiri, Bank Rakyat Indonesia (BRI), and Bank Negara Indonesia, as well as telecommunications company PT Telkomsel. In 2020, LinkAja recorded a 65% new user increase, 250% revenue growth, and quadrupled its transaction volume.

Kaspar Situmorang, BRI’s EVP for digital banking and operation and LinkAja’s board commissioner, shared, “The shift in consumer behaviour and expectations towards digital transactions, added with the disruption from fintechs and startups moving to multi-line and provide their own financial services, should be an extra push for banks to not just transform digitally but also to adapt and be open to coexist with other fintechs and digital platforms”.

In March 2021, Indonesia’s leading ride-hailing platform Gojek announced its investment in LinkAja and raised the total series B funding of LinkAja to $100 million. This followed Grab’s investment in LinkAja in November 2020. The partnerships enable LinkAja as a payment option in Grab and Gojek platforms and provide access to a wider ecosystem and technology. This can propel the e-wallet’s future growth. According to Gojek, combining forces with LinkAja enabled seamless cashless payments experiences across complementary market segments that cover a wide range of user needs. Currently, LinkAja’s platform is largely focused on payments for retail, public services and other daily needs with ~80% of its registered users coming from Indonesia’s tier 2 and tier 3 cities. GoPay serves the payment needs of Indonesia’s retail sector and businesses especially MSMEs as well as daily services within the Gojek platform.

Other international technology companies have also shown confidence in the Indonesian market. In October 2019, Samsung Pay collaborated with Dana and GoPay to integrate the e-wallet services into Samsung phones. In January 2020, WeChat also entered Indonesia through a partnership with CIMB Niaga. International players are required by BI to partner with a domestic ‘Buku 4’ commercial bank in order to receive a licence to operate. Foreign players are also required to connect their payment system with Quick Response Indonesian Standard (QRIS) and use Indonesian currency. Last year, Facebook and PayPal have also expressed interest in the booming payment business with strategic investments in Gojek.

E-wallet players look to expand ecosystems and economic impact

Despite a significant progress in the shift towards cashless, cash is still widely used and financial inclusion remains low for individuals and small businesses. OVO’s Thompson shared, “It is our view that increased investment and collaboration are important to developing the sector; and educating the public towards creating more seamless payment infrastructure is one of the milestones to achieve financial inclusion”. In 2021, OVO is looking to expand its offerings in three major verticals - insurance, investment, and lending. OVO introduced peer-to-peer lending with Taralite after securing a licence from the Financial Services Authority (OJK) last year.

Meanwhile, Gojek has been onboarding more consumers and merchants to share the benefits of the digital economy. Patuwo highlighted, “We are constantly innovating our offering to meet more needs by giving consumers new ways to transact digitally both within and outside the Gojek ecosystem”. The platform has launched new features such as GoPay Feed which allows consumers to send GoPay funds to friends while interacting virtually through texts and emojis. It also recently formed a strategic partnership with Bank Jago at the end of 2020 as a step towards providing digital banking services in the future.

From a bank’s perspective, Situmorang encouraged financial institutions to be more open to collaboration. “Banks should embrace the open banking era by adding more application programming interfaces (APIs) to be easily accessed by e-payment players, fintechs, and other digital platforms. Through API, banks will be able to create an integrated payment ecosystem, tap into the existing ecosystem, and expand access and market to offer their services,” he said.

As more e-wallet players are moving to multi-line businesses to provide financial services, it will be crucial for the industry to strengthen interlinkages among providers to foster a more seamless experience for customers.

As the number of e-wallet players in Indonesia surges amid the vast market opportunities, bigger players have begun extending the competition beyond payments

www.theasianbanker.com

en.antaranews.com

coal is high grade and only economically suitable for steel industry. For fuel coal,

coal is high grade and only economically suitable for steel industry. For fuel coal,  coal low-medium grade is more suitable

coal low-medium grade is more suitable

Kompeni bin Arabia

Kompeni bin Arabia